November Inflationary Trends in Australia

On Monday, the Melbourne Institute (MI) released its monthly inflation gauge, revealing that inflationary pressures remained stable throughout November.

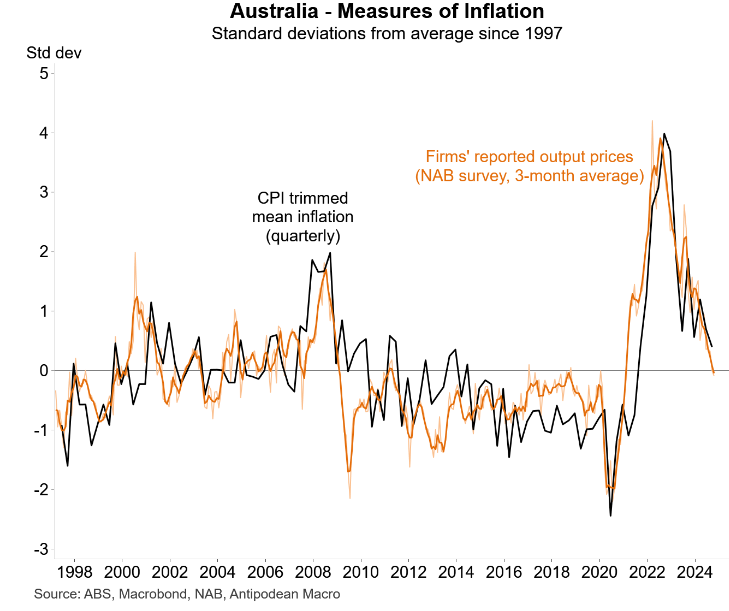

Trimmed Mean Inflation Insights

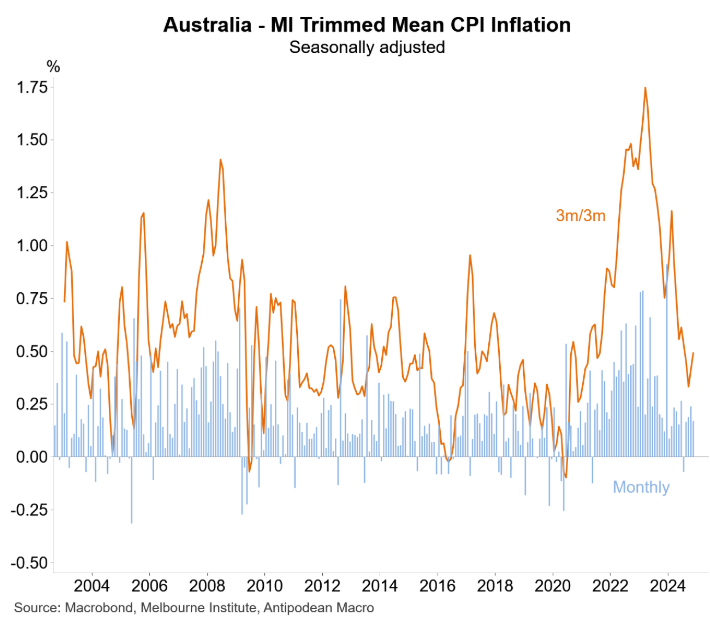

As highlighted by Justin Fabo from Antipodean Macro, the MI’s trimmed mean inflation saw a modest increase of 0.2% in October, but it rebounded to 0.5% on a quarterly scale.

The following analysis from Fabo indicates that “the MI measure of quarterly trimmed mean inflation continued to suggest potential declines in the official measure in the near future.”

Forecasting Future Inflation Rates

Fabo notes, “This aligns with our early forecast for Q4 trimmed mean inflation to be +0.6% q/q, a decrease from Q3’s +0.8% and below the RBA’s Q4 prediction of +0.7%.”

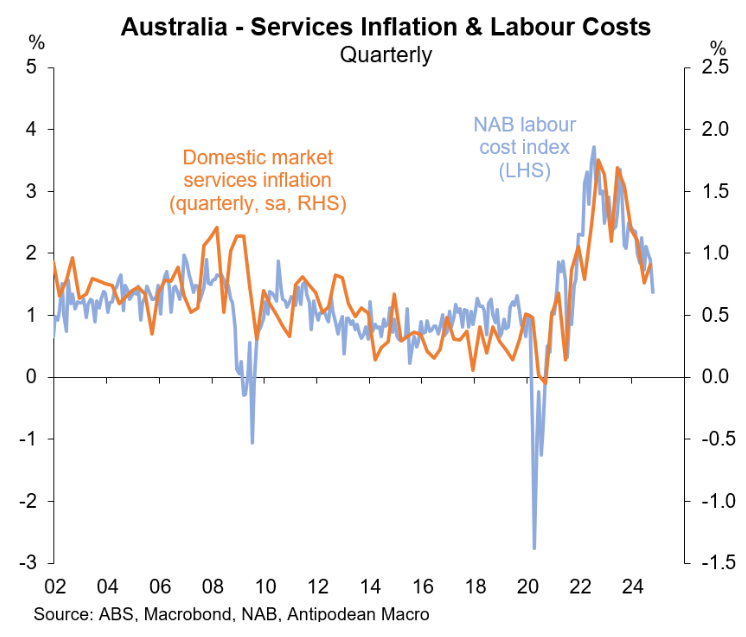

Business Insights on Labour Costs

The recent NAB business survey, published in mid-November, indicated a deceleration in labour cost growth, suggesting that domestic market service prices are likely to experience further disinflation.

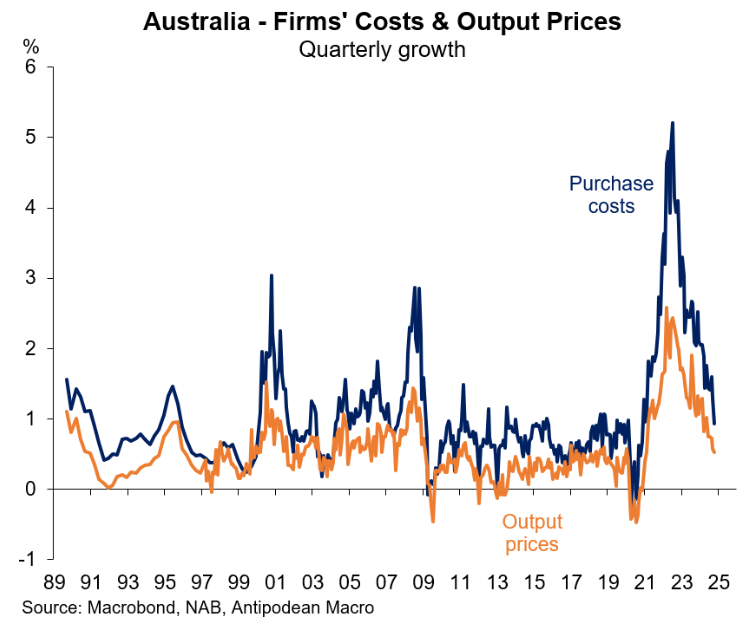

Output Prices and Purchase Costs

Australian businesses have reported a slowdown in the growth of output prices and purchase costs, reverting to levels consistent with the 2000-2019 average.

Implications for Underlying Inflation

This reduction in output price inflation is promising for the outlook on underlying inflation trends.

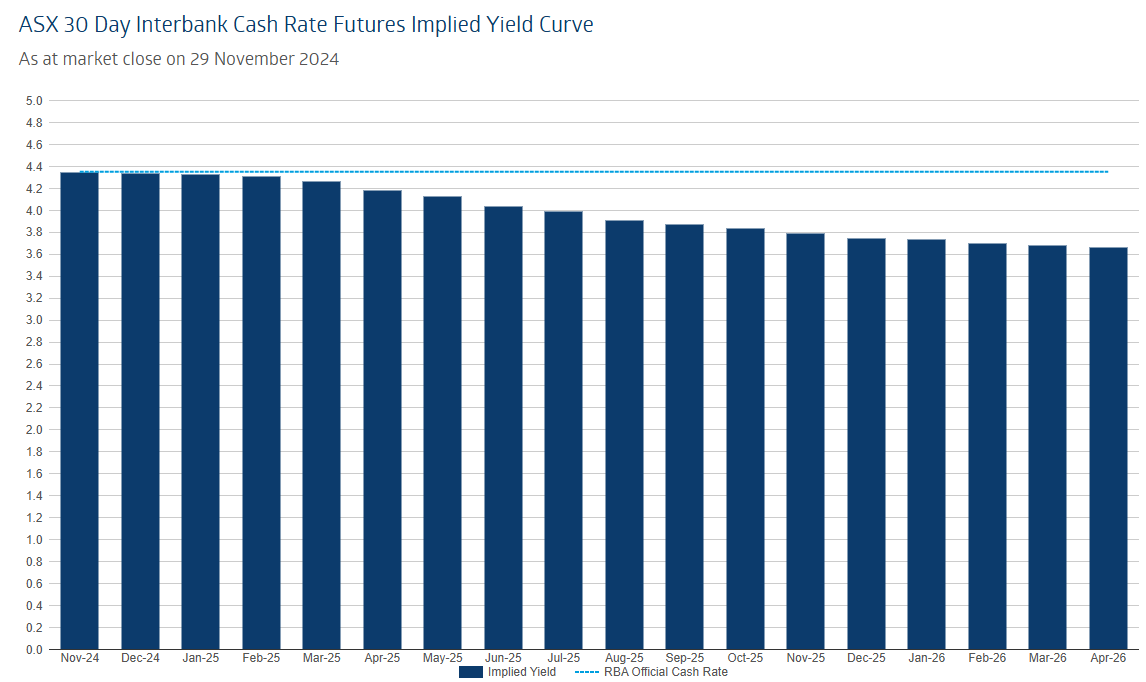

Market Predictions

Financial markets are anticipating potential interest rate cuts in Q2 2025.

Government Expectations

The Albanese government hopes that the trends observed in the MI inflation gauge and NAB business survey will be reflected in the official CPI inflation data, encouraging the RBA to lower rates prior to the May 2025 election.

{kind=link}