The Current State of Australia’s Economy

Recent economic growth figures reveal an unsettling reality — government actions are staving off recession in Australia.

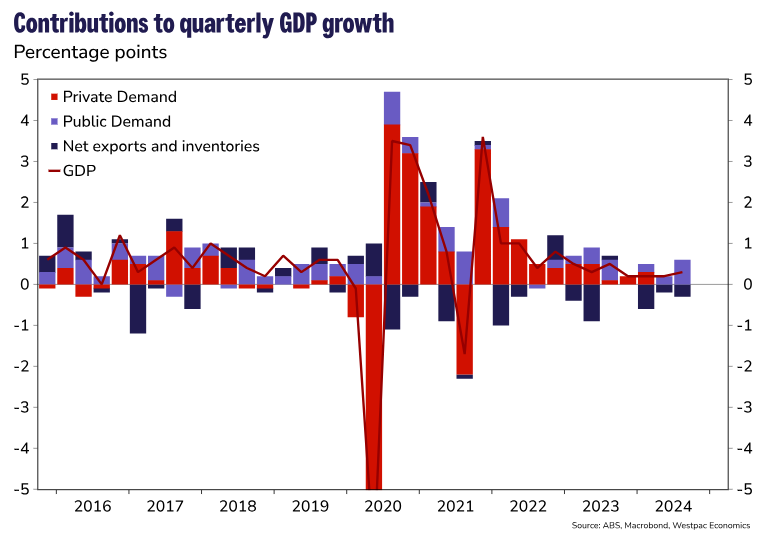

This conclusion is illustrated by a graph from Westpac’s economics department.

(Supplied: Westpac)

Eliminating the contributions from public demand over the last two quarters would have resulted in an economic contraction.

Two back-to-back quarters of negativity in GDP is often described as a recession under conventional definitions.

Although avoiding the term “recession,” Reserve Bank Governor Michele Bullock has subtly acknowledged this reality during recent discussions.

In response to WA Liberal senator Dean Smith’s inquiry about the government’s spending,

Ms. Bullock remarked that her comments were not intended as a caution.

“What I’ve observed is that the private sector in Australia is currently very weak, and the public sector demand has been filling that gap.”

At a recent dinner featuring prominent business and policy leaders,

Ms. Bullock reiterated her defense of government spending amid rising public sector employment.

“If it weren’t there filling that gap, the employment market could be significantly worse,” she argued.

“We’re talking about teachers, nurses, and aged care workers. These roles are essential to our society.”

“I reject the notion that growth in non-market employment is negative; it is, in fact, beneficial.”

Interest Rate Adjustments and Their Implications

However, there’s a twist to this situation.

The Reserve Bank has yet to lower interest rates, believing that the job market remains robust — as evident from an unemployment rate of just 4.1%.

This condition, alongside high demand relative to supply, may be impeding inflation’s rate of decline.

Both the labor market and demand levels are heavily reliant on unprecedented government expenditure, which now constitutes 27.5% of the total economic output.

While it’s clear that interest rates might have decreased by now with less government spending and fewer public sector jobs, the counterpoint is stark: a tighter fiscal policy this year could have thrust Australia into a technical recession and raised unemployment significantly.

According to Gareth Aird, the head of Australian economics at CBA:

“Restrictive monetary policies have effectively curbed private demand growth within the economy.”

“Even with a tax cut boosting household incomes, we didn’t see a considerable rise in consumer spending during the September quarter.”

The Election Discourse and Government Spending Debate

The political ramifications of the GDP statistics serve as a microcosm of the broader economic discussions nearing the federal election next year.

In a bold statement, shadow treasurer Angus Taylor criticized the combination of high public spending and a weak private sector, advocating for the Coalition’s small government philosophy.

(ABC News: Marcus Stimson)

“Labor’s only plan is for a larger government with increased expenditure. The treasurer’s excessive spending is bankrupting Australia,” he stated.

“The Coalition will reinvigorate Australia by boosting investment, enhancing competition, cutting wasteful spending, rebuilding businesses, reducing taxes, and providing secure, low-emission energy.”

Conversely, Treasurer Jim Chalmers pointed out the corrective steps taken by the Albanese government to help control inflation and enhance wages from levels inherited from the preceding Coalition administration.

(ABC News: Ian Cutmore)

“Compensation for employees has risen, leading the labor share of income to increase from 49.3% during the election to 53.5%,” he explained.

“Had our political rivals maintained control, the economy would be weaker, and household finances would face greater strain.”

“They are against costs of living support, advocating for a $315 billion withdrawal from the economy at the worst possible moment — a clear path to recession and increased household distress.”

Government Spending Cuts: Necessity or Risk?

Chalmers posed a challenge to the Coalition in its advocacy for smaller government.

The most significant rise in public investment for the September quarter? A staggering 35% increase in defense spending.

“If the Coalition proposes significant defense budget cuts, they need to express that clearly,” he stated.

Moreover, data from the ABS indicates a surge in state spending as a primary driver of public demand.

According to EY’s Oceania chief economist Cherelle Murphy, much of this investment was planned years in advance.

(ABC News: Daniel Irvine)

“It’s challenging to find a government in Australia that isn’t experiencing record high capital programs for the next four years,” she noted.

This is mainly due to prior commitments on infrastructure designed to support economic stability through the pandemic.

“Moreover, spending demands on the government continue due to an aging population, heightened service requirements, increasing defense needs in a volatile political landscape, and energy transitions.”

The long-standing lack of investment in necessary public infrastructure to accommodate rapid population growth intensifies the stress on transport, health, education, and other essential services.

However, if both major parties recognize defense spending as untouchable, is there public support for reduced spending in transport infrastructure, hospitals, healthcare, disability support, aged care, roads, clean energy, childcare, schools, or higher education?

Labor appears to be banking on minimal opposition.

It seeks to pose a pivotal pre-election question to the opposition, which champions reduced government and lower taxes: “What will be cut to achieve fiscal balance?” and how will that impact an economy so dependent on public sector support for activity and jobs?

At the same time, Labor faces continued scrutiny regarding its plans to energize a sluggish private sector, lessening the burden on the public sector.

“The September National Accounts depict a gloomy economic picture without much optimism,” remarked Cherelle Murphy.

“The private sector needs more than quick solutions to current challenges from their governments.”

The significant query remains whether any party will bring about substantive change in the next election.

{kind=link}